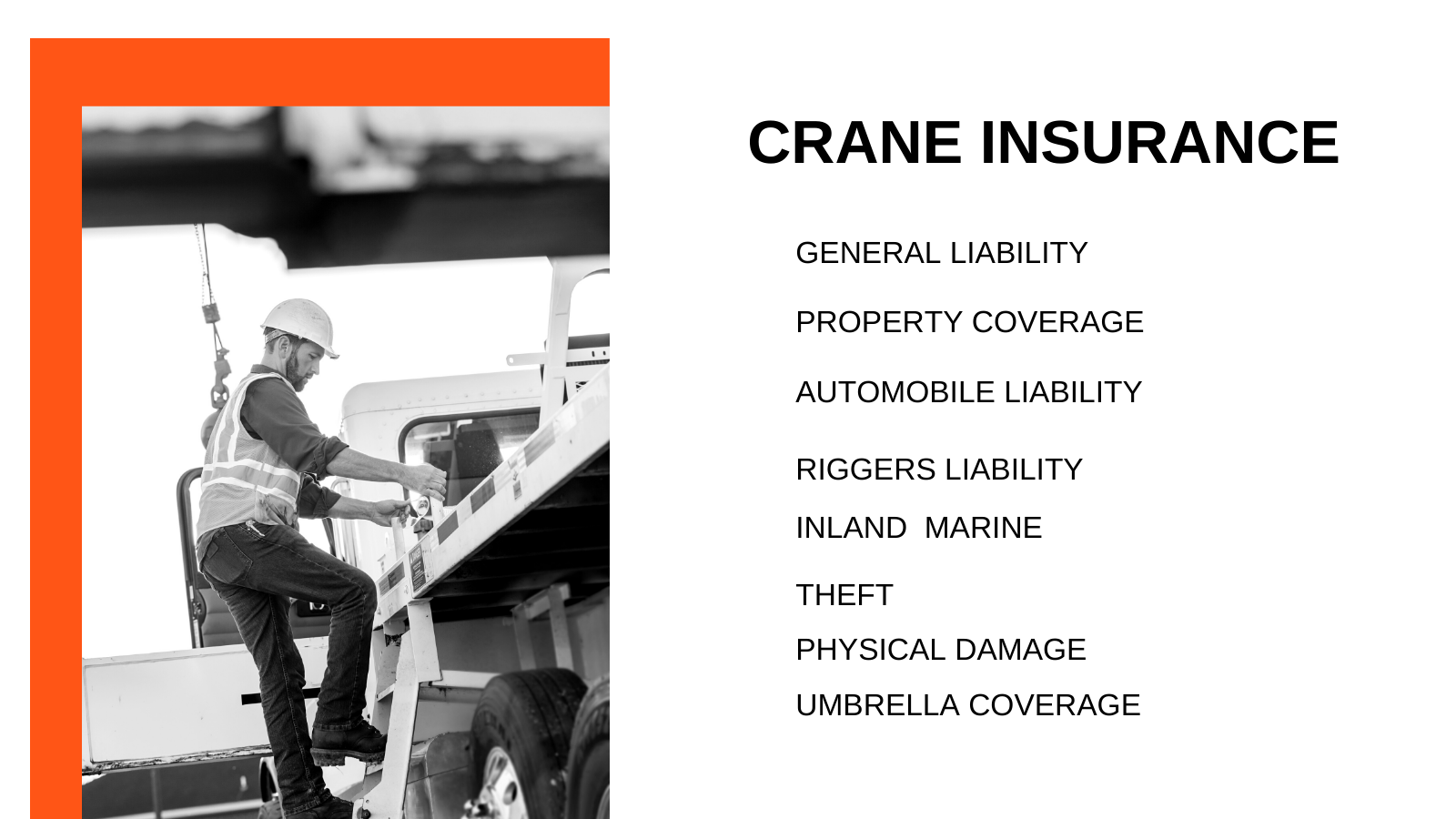

Crane Insurance Coverage Components

If you’re looking for crane insurance coverage, there are key components that you will find available.

Whether you are operating a crane for a specific application (say for a manufacturer or industrial area – or maybe at the port to lift shipping containers) or for the construction industry, statistically, cranes complete challenging tasks and create potentially hazardous work environments.

Your business might have a large or small fleet of cranes. Regardless, the factors that contribute to hazardous conditions for crane operators include:

- The geographic location of the work

- Weather conditions, notably wind

- The terrain on the job site

- The age and maintenance of the crane

- The training and experience of the crane operator(s)

- Safety training

The protection required by crane operators is unique. The kinds of components you will come across for crane insurance include:

- General liability – which protects against injury claims made by a third party or against property damage

- Riggers liability – which covers the personal property of others in your care that you are lifting, hauling, or moving

- Property – which protects your property in the event of a mishap

- Inland marine – which covers equipment that isn’t permanently anchored at a specific location

- Automobile liability – which covers the crane while it’s being transported on public roads

- Theft – which covers the cost of replacing stolen equipment

- Physical damage – which covers up to the full value any damage that affects cranes

- Umbrella – which is a separate policy over and above basic liability policies and intended to cover your business against gaps in coverage

There are other components above and beyond these basics, including:

- Excess liability – which covers lawsuits that exceed the limit of general liability coverage

- Equipment breakdown – which is coverage for some of the issues excluded by other policies, for example, an explosion

- Rented/leased equipment – which ensures you can rent or lease equipment to keep business going if you have to have your equipment repaired

- Business interruption – which covers loss of earnings if your income is affected by equipment failures and repairs

- Equipment floater – which is additional to inland marine coverage and covers equipment while it is being transported between jobs

Do you have further questions about any of the components of crane insurance? Contact New Heights Insurance Solutions, and we’ll happily provide you with more information and your coverage options.